- Subject Code : BAFI1065

- University : RMIT University My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Accounting and Finance

Answer)

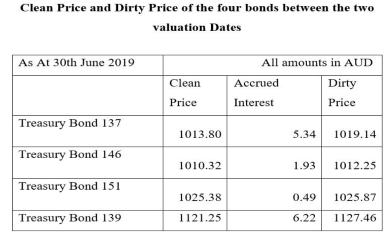

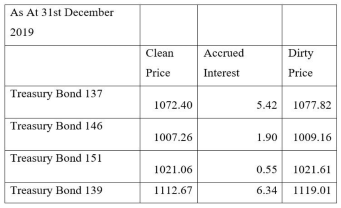

The estimation of dirty price requires the use of coupons in the desired time frame. The flows of cash occurring at different instances of time were discounted to arrive at the present value per period. This value was then added to arrive at the price on the time instances in question. The estimation of the price of bond had to be done in the course of coupon period. Thus, it(bond) value is judged and found in the commencement of the time frame. It is then compounded forward to the date when the pricing is to be determined. The interest accrued was computed by computing the days starting from the last coupon date and the date on which pricing is to be estimated. This method helps in determining the clean prices.

The notion of calculating the clean & dirty prices hold much importance in pricing of bond. The clean prices are ones in which are exclusive of the interest that has been accrued. However, in case of dirty prices, it is inclusive. The bonds in theory can be valued on coupon daets but in the practical world they can be traded(bought and sold) on a different date or time. Therefore it becomes imperative to adjust the interest that has been accrued on the bond. The person who is selling the bond will thus make payment of the dirty price i.e. the clean price and the interest. The one purchasing the bond will thus get the cash flow relating to coupon on the next scheduled date. Thus in theory, the price of bond in the market is the one which has both clean price and interest. Once the coupon payment is made then the clean price will be equivalent to the dirty price.

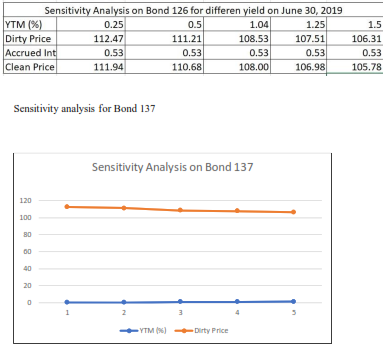

Sensitivity Analysis

Sensitivity analysis is the tool used in the estimation of behaviour of output variables depending on the changes occurring in input variables. They are used as financial and mathematical model. By the use of this method we try to determine the what if scenarios in the market. This model tries to find out and simulates the outcomes wherein the range of variables is given.

Answer)

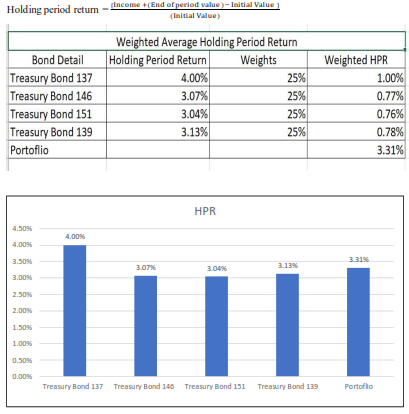

Holding Period Return

Holding period return(HPR) is the return which is gained when a stock/asset or a bunch of assets are held by a person for a scheduled time frame. The time frame for which the person is in possession of the assets is called holding period. This time frame is in normal cases shown as a percentage. The calculation and estimation of Holding period return is established on total returns that have been gained from the stock/asset or a bunch of assets held, which includes the income from the held assest and the change in price/value. This method holds a lot of importance when the stock/asset or a bunch of assets are held by a person for different time frames.

The above discussion about the holding period return shows that there is a significant difference in the yield of HPR and YTM(yield to maturity). The reason for this is the time frame for holding period is not same as the time frame for YTM. In the former case the asset class can be sold on any date whereas in case of the latter the asset has to be kept in possession till it matures. Thus, in former case the return gained will be dependent on the fact that for how many days the asset was in possession, so the yield also depends on the same. This method is also utilized in the comparison of asset/bonds having variety of maturity dates and dissimilar yields. This method also helps the traders and investors to find the best performing bond/asset. It can also determine the profit it is making, and the length of time it should be held to generate the

amount of profit determined previously. This method assists in balancing the bunch of assests in possession to maximize profit. It provides assistance in computing whether the bond should be sold in the scheduled time frame at a premium or should be kept in possession till it matures. It thus finds out the best case scenario. The period of holding in this answer has been accounted as 6 months. It is assumed that the bonds taken into consideration in previous questions were bought on 30/06/19 and sold on 31/12/ 19. The holding period return is highest for bond 137 and lowest for bond 151. Let us assume that equal amount is invested in all these four bonds then the return percentage comes to 3.31%. This is higher than the individual returns of the most bonds.

Answer)

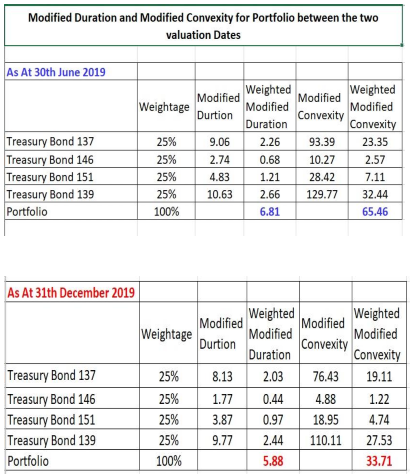

Modified Duration

When the interest rates vary then there is some change in the price of bond. This variation can be computed with the help of Modified duration. Thus, it tries to evaluate the variation in the prcie of bond vis-a-vis interest rates. The prices are sensitive to interest rates. Evidence suggests that the bond prices move in inverse direction of interest rates. This method determines the effect upon the price of a bond due to a 1 percent (or 100 basis point) change in interest rates. Calculated as:

Modified Duration = (Macauley Duration)/(1+YTM/n)

Where:

Macauley Duration = weighted average term to maturity of the cash flows from a bond

YTM = yield to maturity

n = number of coupon periods per year

Convexity

The prices of the bonds and their yield are related to each other. When they are plotted on a graph against each other, they form a curve pattern. The curvature of this graph is known as

Convexity. This also exhibits the variation in the duration of bond fluctuation in the interest rates. This is employed in the management of risk. It also quantifies the interest rate of the portfolio .

The weighted modified duration for the portfolio is higher on 30/06/19 in comparison to the weighted modified duration on 31/12/19. In the former case it is 6.81 and in the latter it is 5.88. This shows that Bond prices are inversely related to interest rates.

As shown in the above table, Bond 139 has the highest convexity and Bond 146 has the lowest. If assumption is made that all the other things are equal then, Bond 139 will be priced higher than Bond 146 when there is significant positive or negative variation in the interest rates.

Let us assume that there is a bond which has coupon rate of 5% PA. In a scenario where the interest rates show escalate above 5%, the holder of the bond will want to sell it because it is giving lower returns. They will want to invest in some other instrument which will give higher return for example some new bonds. This proves that the price of the bond is inversely proportional to yield to maturity. As the date of maturity nears, the yield shows slackening.

PART 2:

Answer)

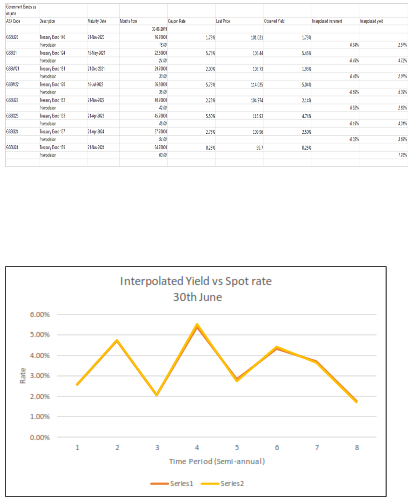

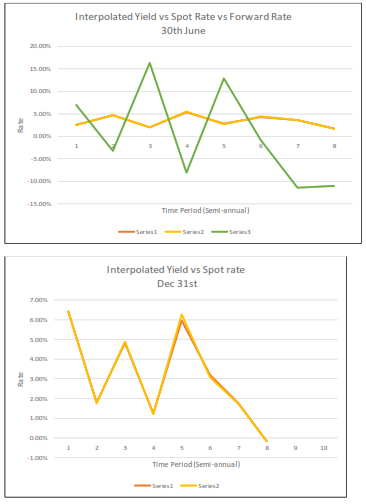

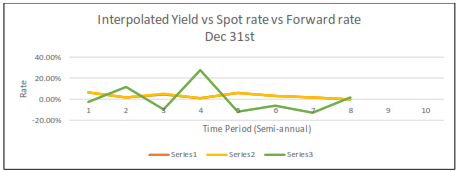

Yield Curve, Spot Curve, and Forward Curve

When the interest rates of various bonds having different maturities are plotted on a graph, taking interest rate on one axis and maturity on the other at a given instant in time. The curve obtained is called yield curve. The bonds awhich are taken into consideration in the above case have homogeneous credit quality The slope computed for the curve formed in above case helps in the determination of variation of economic activity vis a vis interest rates.

The spot curve is constructed with the help of spot rates hence the name. It computes the yield that is utilised in disciounting a single cash flow at a given instance. Theoretically, if the slope of spot curve shows elevating gradient, then similar thing will be noticed when we plot the par curve.

The curve denoting the prices at which execution of contract can be done in current time is called a forward curve. In reference to the above scenario, the forward rate curve changes its direction from an initial direction of upward-slope to a downward one at a later stage. This is shown in the diagrams below. (on 30 June and 31 Dec 2019).

Answer B)

Yield to Maturity, Forward Rate, Spot Rate

The forward rate is a tool that measures the price of an asset at an instance which lies in future. Generally, the contract or the agrreement is done in the present date. The price is agreed upon by the parties involved and delivery of the said asset will be happening in future. The time frame for delivery may happen in near future that is in a few days or in late future example, in a few months. The forward rates are specifically utilized in case of Treasury bills.

The forward rate can be utilized in judging and computing the future spot rates.

There are two theories in which classification can be done. One is the expectation theory and the other is market segmentation theory. The former theory that is the expectation theory can be analysed in three ways. It states that there is a significant relation in the forward rates and projection about short term rates.

This theory can be comprehended and analysed in the below given ways:

-

Pure Expectation Theory construes the fact that the forward rates portray the interest rates in future in an absolute and unprejudiced manner. (Heaney studied this fact in 1994). The fallibility of this approach lies in the fact that it does not take into consideration the inherent risks. Various risks are associated with diverse investment strategies. An example of such risks can be price & reinvestment risk.

-

Liquidity Theory: This proposition propounds that the forward rates are not unprejudiced. This is due to the fact that the people participating in the market will insist on getting a liquidity premium because the long term assets/stocks/securities are uncertain in nature. (Afanasenko et al. 2011)

-

Preferred Habitat: In this theory a proposition is propounded that the calculation of forward rates favour the existence of premium. (Afanasenko et al. 2011). But as in case of liquidity theory, it was propounded that the risk premium caries in a uniform manner vis a vis maturity, this theory does not support the above-mentioned statement. (Fabozzi 2013, p. 127). This approach assumes that the participants in the market insist on premium because of movement from their desired investment options.

The market segmentation theory propounds that the participants of the market will not prefer to change the time frame of their investments even in the case of their getting profits. This profit is generated by forecasting and projection of future spot rates vis a vis forward rates.– (Fabozzi 2013, p. 127).

There are fats that prove that future spot rates rates can be envisioned by studying and analysing the forward rate. This is true in case of short-term maturities (1 month). However in case of bonds having maturities longer than that, this proposition does not stand true (Fama 1984). In the paper by Campbell and Shiller in 1991, they adopted a vector auto regression approach to check the validity of the term structure with observed US Treasury bill data. The study conducted by them also denoted that above mentioned statement holds correct for short term instruments. Again it doesn’t hold good in case of long-term instruments/assets/bonds (Afanasenko et al. 2011).

There are other studies such as one conducted by (Buser et al. 1996) which computes forward rate and adjusts it for biases and risk premium. Buser et al. (1996) suggest that forward rates between 1963- 1993 which have been calculated with relevant adjustments are in fact a good estimate for future spot rates.

The above-mentioned conclusions of the study are refuted by other researchers whose conclusions are different (Fama in 1984 and Cambel and Shiller in 1991. Assumption made in the theories that one single yield can be utilized for discounting is incorrect in real life situations and thus causes wrong estimates. The theories should account for the unnoticed reinvestment risk and risk premium.

The forward rate can be calculated using one of two metrics:

Yield curve – The relationship between the interest rates on government bonds of various maturities

Spot rates – The assumed yield on a zero-coupon Treasury security

The yield curve is the most commonly used tool to estimate the forward rate as compared to spot rates. It has more clear indications of current and future market trends and the estimation of rates and prices.

The spot rate shows the yield for a time frame. Market spot rates for certain terms are equal to the yield to maturity of zero-coupon bonds with those terms. Normally speaking, the elevation in the spot rates also elevates as the time frame. But this is not always the case. Thus, bonds which have maturities in later time frame will have elevated yields as compared to ones having closer maturities.

Yield to maturity (YTM) is the total return anticipated on a bond if the bond is held until it matures. Yield to maturity is considered a long-term bond yield but is expressed as an annual rate. In other words, it is the internal rate of return (IRR) of an investment in a bond if the investor holds the bond until maturity, with all payments made as scheduled and reinvested at the same rate.

References:

1) Afanasenko, D. Gischer, H. & Reichling, P. (2011). The Predictive Power of Forward Rates: A Re-examination for Germany. Investment Management And Financial Innovations, 8(1), pp. 125-139.

2) Australia. ASX., (2020). Interest Rate Security Prices Bonds. Available on: https://www.asx.com.au/asx/markets/interestRateSecurityPrices.do?type=GOVERNMENT_BOND

3) Australia. ASX., (2020). List of Government Bonds. Exchange-traded Treasury Bonds. Available on: https://www.asx.com.au/products/bonds/list-of-agbs.htm

4) Barnard, B. (2017). Rating migration and bond valuation: ahistorical interest rate and default probability term structures. Available at SSRN 2948352.

5) Burgess, N. (2016). Par-Par Asset Swap Spreads: An Illustration of How to Price Asset Swaps. Available at SSRN 2809111.

6) Buser, S.A. Karolyi, G.A. & Sanders, A.B. (1996). Adjusted Forward Rates as Predictors of Future Spot Rates. Journal of Fixed Income. 6. pp.29-42

7) Dong, J., Korobenko, L. and Deniz Sezer, A. (2020). A variation of Merton's corporate bond valuation model for firms with illiquid but observable assets. Quantitative Finance, 20(3), pp.483-497.

8) Fabozzi, F.J. (2013). Bond Markets, Analysis, And Strategies. Boston: Pearson

9) Fama, E.F. (1984). The Information in the Term Structure. Journal of Financial Economics. 13( 4). pp. 509-576

10) Gargano, A., Pettenuzzo, D. and Timmermann, A. (2019). Bond return predictability: Economic value and links to the macroeconomy. Management Science, 65(2), pp.508-540.

11) Georgiev, G. (2017). Calculating Clean And Dirty Price In Interest-Bearing Bonds And Quoting Systems. New Knowledge Journal of Science, 6(1).

12) Gottschalk, S. (2018). A closed-form formula for pricing bonds between coupon payments. arXiv preprint arXiv:1801.06028.

13) Handforth, F., Bland, E. M. and Riley, N. F. (2016). Estimating modified duration and convexity for income properties. The Coastal Business Journal, 15(1), p.1.

14) Homaifar, G. A. and Michello, F. A. (2019). A generalized algorithm for duration and convexity of option embedded bonds. Applied Economics Letters, 26(10), pp.835-842.

15) Kim, G. H., Li, H. and Zhang, W. (2017). The CDS‐Bond Basis Arbitrage and the Cross Section of Corporate Bond Returns. Journal of Futures Markets, 37(8), pp.836-861.

16) Mangiero, G. A., Qayyum, A. and Cante, C. J. (2019). An excel-based method to enhance the study of “Duration and Convexity” in financial management education. Journal of Education for Business, pp.1-6.

17) Melik-Parsadanyan, V. (2016). The Arithmetics of Par, Spot and Forward Curves. International Journal of Economics and Finance, 8(12).

Remember, at the center of any academic work, lies clarity and evidence. Should you need further assistance, do look up to our Accounting and Finance Assignment Help

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start