- Subject Code : BSBFIM801

- University : TAFE My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Accounting and Finance

Question 1

To establish the capacity of the financial system it is very important to first acknowledge the meaning of the financial system and what is it meant to be. The answer to the first question is simple that a financial system is a framework of institutions including banks, stock exchanges, and insurance companies that allows and avails the exchange of funds. But the second question is a little tough to answer which asks that what is a financial system for? And how does it contribute to the national or global economy?

Now, there is no doubt that the financial system employs tons of professional with high-paying jobs and employment figures are the lynchpin to determine the trend of the economy. However, a further question arises is that are they being paid for creating any kind of material service or good. The answer is no, the financial system is not a creator, but just a middleman, that connects the creators with the consumers. And the best middleman is the one that is the cheapest and most efficient at the same time.

The existing financial system is a bloated parasite. In the 1960s, the US financial system used to provide 6.2% of overall employment and 14.5% of overall earnings. These two figures doubled between 2004-2014. No doubt, there is finance and IT advances in these last five decades, but how it can become twice when the job remains the same as a middleman?

Question 2

The important business processes for successful business performance management (BPM) systems includes planning, forecasting and budgeting

Planning

Outlines the financial direction of a company and creates appropriate models of management’s expectations for the upcoming financial periods. The process of planning is generally the initial step in setting up a company and the decision-making process while investing.

Budgeting

It documents the overall plan that is going to be executed on a month to month basis. It typically conducts estimations about expenses & revenue and expected debt reduction & cash flow. Companies generally set-up their budgets as the calendar or fiscal year begins, also ample room is left for adjustments as expenses or revenues might decline or grow. The budgets prepared are finally compared with actual financial statements at the end of the proposed period for evaluating the variances (or errors) between the two.

Forecasting

This process typically uses the market conditions and accumulated historical data for predicting the possible financial outcomes in future periods. The main aim of forecasting the future is to help the management in anticipating the results based on past information.

Question 3

The four main types of forecasting methods that are used by financial analysts to predict future expenses, capital costs and revenues for business are:

-

Straight-line Method

The straight-line method (SLM) is a simple forecasting method that financial analyst uses, they employ trends and historical figures to predict future revenue growth.

-

Moving Average

Moving averages (MA) is a smoothing technique that identifies the underlying pattern of the data set for establishing an estimate about future values. Generally used moving averages include the 3 months and 5 months MAs.

-

Simple Linear Regression (SLR)

The regression analysis is a sophisticated statistical tool to analyze and establish a relationship between two variables for prediction. One variable is known as the dependent and the other is known as the independent variable.

-

Multiple Linear Regressions

This is a modified version of SLR and is typically used to forecast future values when there are two or more independent variables are available for projects.

Question 4

The important business processes for successful business performance management (BPM) systems includes planning, forecasting and budgeting.

Planning

Outlines the financial direction of a company and creates appropriate models of management’s expectations for the upcoming financial periods. The process of planning is generally the initial step in setting up a company and decision-making process while investing.

Budgeting

It documents the overall plan that is going to be executed on a month to month basis. It typically conducts estimations about expenses & revenue and expected debt reduction & cash flow. Companies generally set-up their budgets as the calendar or fiscal year begins, also ample room is left for adjustments as expenses or revenues might decline or grow. The budgets prepared are finally compared with actual financial statements at the end of the proposed period for evaluating the variances (or errors) between the two.

Forecasting

This process typically uses the market conditions and accumulated historical data for predicting the possible financial outcomes in future periods. The main aim of forecasting the future is to help the management in anticipating the results based on past information.

Question 5

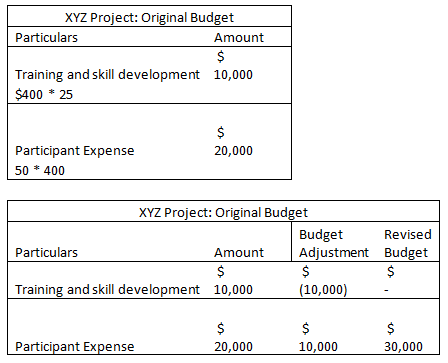

There might occur some differences due to the time gap between the submission of a proposal and its final approval. Therefore, the budgeted costs might require to be revised. For example, an XYZ program requires a line item budget for an Employee Training Workshop for $10,000 to be conducted by the local skill development and educational department. Later, the department waived all the fees and announces that training will be free of charge. Now there will be the unrealized amount of $10,000 that has been specifically reserved for the training course. The program later identified 200 migrant labours that can be benefited from attending XYZ skill course for $50 per attendee. In this situation, a budget revision will be required.

Question 6

The balance sheet of a company is also known as the positional statement. It determines the liabilities, owners' equity and assets of a firm. As a shareholder or a potential investor of a company, it is crucial to understand the structure of a balance sheet and ways to read and analyze it. The main equation of balance sheet is:

Assets = Liabilities + Shareholders' Equity

To analyze the balance sheet, an important technique is financial ratio analysis. It uses quantitative formulas to discover the insights of a company’s management and its operations. It can help in determining the financial health of a company, and its operational efficiency. The largely used balance sheet ratios that use information from a positional statement are:

-

Financial strength ratios: it includes working capital and debt-to-equity ratios, which provides information about the capital structure of the company and the capacity of the company to meet its obligations.

-

Activity ratios: It mainly focuses on current accounts and aims at determining the efficiency of the company in managing its operating cycle, which includes inventory, accounts payables and receivables.

Question 7

A human being is a social animal and it can only survive if it lives in a community. But, as a member of the community, the humans are required to fulfil their part of duty, one such kind of moral obligation or duty is to protect the children from reasonably foreseeable harm and keep them under supervision and care. The organizational staff of a schooling institution has been consulted to establish the management responsibilities and legal requirements for reporting.

School staff members play a very crucial role in protecting children and they are required to comply with a range of legal and moral obligations in relation to identification, response and reporting of child abuse. One of the simplest methods to comply with the legal and moral obligations is to make it a practice to remember and report any material suspicion In relation to child abuse, or is at risk of being abused.

Question 8

The analysis and interpretation of financial reports are very important for the stakeholder’s of the company including shareholders, prospecting investors, government agencies, creditors, etc. to make proper decisions. The process of analyzing the financial statements and other reports including the director’s reports, auditor’s reports, remuneration report, etc. for decision-making purposes is known as financial statement analysis. The stakeholders use such analysis to understand the overall financial health of a business, to evaluate its financial performance and to value the business.

In general, the most important part of a financial report is the financial statements that are prepared based on AASB or GAAP or IFRS norms. As per accounting standards, the business is essentially required to prepare and maintain three important financial statements including the income statement, the balance sheet, and the cash flow statement.

The analysis of financial reports commonly utilizes several techniques. The most important methods that are generally used include the vertical analysis, the horizontal analysis, and the ratio analysis. First Horizontal analysis makes a horizontal comparison of the data, by analyzing figures across multiple financial periods. The vertical analysis focuses on vertical impacts of one line item on others and also evaluates the business’s proportions. The ratio analysis is the most important that calculates important ratio metrics and measures statistical relationships.

Question 9

The elementary success of a financial strategy mainly depends on the below mentioned three important factors:

-

The alignment of form with the external environment,

-

Firm’s rational internal view of its foundational competencies and

-

Competitive advantages those are sustainable. Its careful implementation and proper monitoring.

An entity must know their goals and how to achieve them. And the strategic-planning process uses data-analytical models that are capable to provide a practical picture. The process includes five distinct steps as mentioned below to enable a firm in performing activities differently and innovatively from its rivals and competitors or in performing activities in a more efficient manner. The decision-making process and strategic-planning process includes:-

-

Vision Statement

-

Mission Statement

-

Analysis

-

Strategy Formulation

-

Strategy Implementation and Management

The introduction of the balanced scorecard (BSC) has emphasized the performance of a firm as important indicators. It helps in linking the strategically determined goals to actual performance. It provides timely, useful and material information to facilitate operational and strategic control decisions. This has led to the role of finance in the strategic planning process becoming more relevant than ever.

Question 10

Budgeting documents the overall plan that is going to be executed on a month to month basis. It typically conducts estimations about expenses & revenue and expected debt reduction & cash flow. Companies generally set-up their budgets as the calendar or fiscal year begins, also ample room is left for adjustments as expenses or revenues might decline or grow. The budgets prepared are finally compared with actual financial statements at the end of the proposed period for evaluating the variances (or errors) between the two.

The process of budgeting forms a basis towards the success of a business. It helps a firm in controlling, planning and financial decision making. Without control over expenses, the planning must be futile and in the lack of proper planning, the business will not be able to achieve any business objective.

A budget includes proper planning in relation to:

-

Controlling the business’s finances

-

Ensuring that firm can fund its current obligations

-

Make the firm able to meet its desired objectives and make financial decisions confidently in the benefit of the business; and

-

Make sure that the firms have an ample pool of cash to finance future projects.

Question 11

The process of a good negotiation is to understand the interest of other parties while not putting owns interest at cost. There it is very important to choose an appropriate strategy that best responds to the interests of both the parties and with proper tactics, a business will be able to achieve the best outcome. The strategy must be selected based on the prevailing situation and can be changed or modified while in the negotiation process. Some of the important negotiation strategies include:

-

Problem-solving: The parties on both sides are committed to examine and discuss the issues closely before entering into a long-term arrangement that requires scrutiny

-

Contending: persuasion of the negotiating party to concede to your outcome, when bargaining over major 'wins' or in one-off negotiations.

-

Yielding: yield a point that is not important to you, but is crucial to the negotiating party; it becomes valuable during ongoing negotiations.

-

Compromising: both the negating parties forgo their outcomes to some extent, and settle with an outcome that is mutually satisfactory for all the participant

-

Inaction: It buys time to discuss and rethink about the project or proposal, the borrowed time is consumed in gathering larger information and makes decisions about further tactics.

Question 12

The budgeting process and resource allocation are the most important and powerful components in the business planning process. The term resource allocation refers to the proper distribution of resources, with particular financing that ranges from the centre to lower levels. The budgeting process implies to the detailed determination about how the firm’s budgeted funds are going to be utilized.

A better financial management process and systems to track the resource allocation and utilization are essential at the departmental level for effective utilization of the resources. Effective financial control and planning will help departments to:

-

Ensure the efficient and effective use of resources

-

Make sound business decisions

-

Demonstrate accountability

-

Take remedial action where needed

Budget estimates expenditures and revenues for a specific period of time. Therefore, it must not be considered as just an accounting document but as a planning and management tool. It assists the firm in the better and efficient allocation of resources. Budgeted allocation is the designated amount of funding to each expenditure item. It also specifies the max amount of funds that a firm wants to spend on a specified program or project, and also provides a limit that must not be exceeded by the managers to whom the funds have been allotted and are authorized to spend.

Question 13

Management Information Systems plays a significant role in the development of organizations. The impact of information systems on the financial sector like banks and other service industry is vital. MIS is the study of technology, people, the businesses and the relationships exist among them. The system professionals help a firm in realizing the maximum possible benefit from making investments in business processes.

Senior leaders of an organization need more skills than before to understand the complexity of information management, not only to understand soft and hardware but also social media which is becoming an import subject in today’s business and social life’s. Understanding information governance is one of the elements which should be high on the agenda by any kind of organization dealing with customers. Today business leaders should be aware of the changes which occur daily in information management. Is the change important for an organization and are employees willing to change, confirming new rules and regulations? Decision making, creating storage, archiving and delete information to ensure internal process, roles and policies are just a few vital standards of effectiveness and efficiency within the organizations. Critical analysis will be highlighted to discuss ethical decisions made by senior leaders, whereby the new law of customer protection of information sharing is secured to create a save environment for customers and companies.

Question 14

The budget that reflects the allocation of resources and their outcomes of services at the departmental level of an organization is known as performance budget. The goal is to score and identify relative presentation based on target attainment for particular outcomes. Such budgets are generally used by governmental agencies or bodies that represent a link between the outcome of services serviced by local, state, or federal governments and the taxpayer funds.

However, the budget represents a substantial amount of important material information and data, but it is not able to offer any marginal information related to the variances of the budget or budget deviations. The marginal information is not necessarily required to be of financial nature that means it can be non-budgetary information. The marginal costs used to acquire the resources or weak conditions of economy are the essential factors that are required to be considered before budget approval. Changes in regulations or laws or government policies that are related to business can substantially impact the budget and the related information. Hence, a performance report is required to be provided for ensuring no surprises or contingencies in the future.

Question 15

The process of auditing is an important compliance process that aims at ensuring the financial statements of an entity are fairly prepared and properly presented by complying the guidelines of accounting laws and standards (AASB in Australia). The auditing of financial statements is an independent and systematic investigation of statutory documents, vouchers, books of accounts, records, etc. of a business firm. Auditing is typically conducted by the management of the company by hiring an external independent auditor or auditing firm as per the prescribed laws for ascertaining the fair and true picture of the non-financial disclosures and financial statements of a company.

For an audit to be considered as a quality audit procedure, it should be performed by a qualified and independent entity or person as per the auditing standards (Australian Financial Review, 2020) or domestic GAAP. The top global level auditing firms include the PwC, Ernst & Young, Deloitte and KPMG and is collectively known as the big fours accounting firms. These firms are considering being most qualified entities based on their reputation and size for the auditing purpose. However, evidence has been presented by ASIC that the audits performed by these big 4 auditing and accounting firms are incompetent to assure the accuracy and authenticity of the financial statements.

Question 16

Financial risk factors form the basis of investing and helps in identifying the systematic returns in financial markets, and the possibility of losing money. Lyxor provides a Five-Factor Framework on the unconventional risk:-

-

Low Size Factor: It refers to the phenomenon that small-cap and mid-cap securities outperform the large securities over time and the benefit can be calculated using market capitalization.

-

Value Factor: It states that inexpensive securities relative to some measure of fundamental value tend to outperform the costlier securities. It allows a better return in case their current price is lower than their current value.

-

Low-Risk Factor: Low volatility or low-risk securities, with low market leverage, tends to outperform over time as compared to securities with higher market leverage and higher volatility.

-

Quality Factor: It states that high-quality securities with stable earnings, stronger balance sheets, higher margins and growing profits tend to outperform the securities with low-quality, which are unprofitable and indebted overtime.

-

Momentum Factor: The momentum factor refers to the tendency of securities that it will continue to rise if they have witnessed a consistent rising trend in the past, and for falling share prices to keep falling.

Question 17

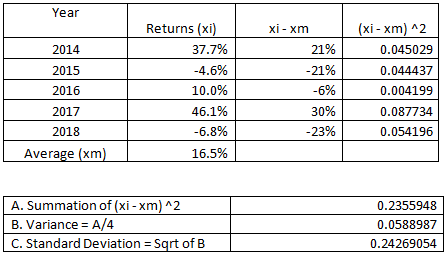

In the financial sector, the management of risk is a continuous process to identify, analyze, mitigation or accept the possibilities of uncertainties in investment decisions. Risk management occurs when a fund manager or an investor makes efforts to quantify the likelihood and potential for the losses in a proposed investment, and then takes required action given the risk tolerance and objectives.

Consider shares of a hypothetical Stark Int. for the last 5 years. Returns for Stark’s stock were as follows:

So the risk associated with shares of Stark In. is approx 24.3%.

Good documentation is an important factor in the successful risk management process. The below list is can give an idea about risk documentation requirements:

-

Risk appetite statement

-

Risk management framework

-

Risk materiality

-

Risk register

-

Risk taxonomy

-

Risk charters and mandates

-

Risk management policy

-

Methodologies

-

Risk escalation process

-

Risk metrics

-

Risk communications

-

Risk training course

Question 18

Financial risk is typically related to leverage and businesses are getting highly sophisticated in managing financial risks, which is the key to their survival. The problem is that the companies are required to manage various risk due to exposure in a globalised economy which is not limited to only credit risk, currency risk or interest-rate risk, but also an operational risk, equity risk, insurance risk, cross-border risk and legal risk.

The complication in the business financial risk management not only demands progress in the main activities but also requires the evaluation of the financial health of the companies. So that the business risk does not remain limited but also include risks like operational risk, insurance risk and capital risk. The vital questions that are required to be answered by the risk management department are:

-

Whether all the available resources have been effectively used,

-

Whether the firm remains profitable and whether the business objectives met or whether they exceeded the management’s expectations, and

-

Whether financial decision making was done carefully.

As the equity markets all around the globe are integrating at a face pace therefore it is essentially required to bridge the information gap exists in the international reporting of financial statements using domestic GAAPs. IFRS has provided a uniform code for accounting standards and the global business communities are converging their national GAAPs into IFRS

Question 19

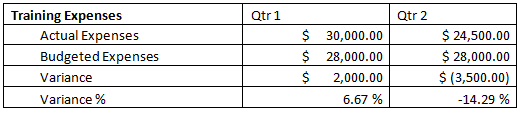

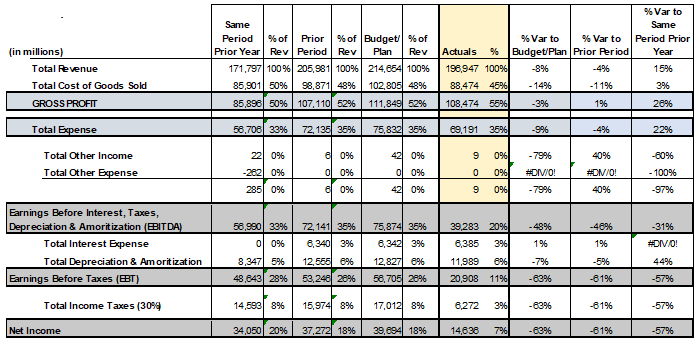

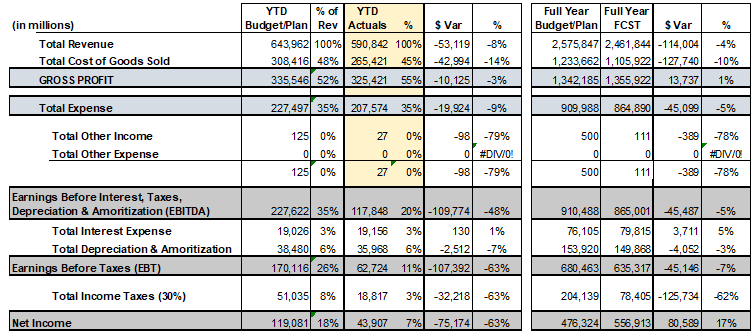

Budgeting documents the overall plan that is going to be executed on a month to month basis. It typically conducts estimations about expenses & revenue and expected debt reduction & cash flow. Companies generally set-up their budgets as the calendar or fiscal year begins, also ample room is left for adjustments as expenses or revenues might decline or grow. The budgets prepared are finally compared with actual financial statements at the end of the proposed period for evaluating the variances (or errors) between the two. There might occur some differences due to the time gap between the submission of a proposal and its final approval. Therefore, the budgeted costs might require to be revised.

For example, the operating budget of a firm is forecasting training expenses. Assume two quarters in a budget cycle, the budget and variance analysis is:

Question 20

A very important step in the financial planning and analysis (FP&A) process is to prepare a budget report, perform a variance analysis with actual figures and analyze the reasons for the variance. Variances fall into two major categories:

-

Favourable variance: Actual figures are better than the budgeted.

-

Better than expected result

-

Costs lower than expected

-

Revenue higher than expected

-

-

Negative variance: The actual figures remain worse than the budgeted.

-

Worse than expected result

-

Costs higher than expected

-

Revenue lower than expected

-

When explaining budget to actual variances, it is a best practice to not to use the terms “higher” or “lower” when describing a particular line time. For example, expenses may have come in higher than planned, but that produces a negative variance to profit.

1. The classic budget to actual variance

2. Variance to prior period and same period prior year

3. Year-to-date (YTD) and forecast

Question 21

A budget is prepared to propose planning for the expenditure on a project, proposal or portfolio. It develops the foundation through which the predicted eventual cost of the work is compared with that of actual expenditure and finally reported.

The Initial estimations of cost are based on parametric or comparative techniques. These are defined as the desirability and achievability of the work for investigation purposes and thus a detailed understanding of schedule, resource and scope is developed.

The base cost is generally made up of various costs associated with the following:

-

resources such as staff or contractors;

-

accommodation and infrastructure such as office rental or support for ICT systems;

-

consumables such as power or stationery;

-

expenses such as staff travel and subsistence;

-

Capital items such as equipment purchase.

These base costs have two pairs of possible attributes:

-

Direct and indirect: costs that are directly attributable to the project, program or portfolio are direct costs, whereas overheads shared with other parts of the host organization are indirect.

-

Fixed and variable: fixed costs remain the same regardless of how the work precedes, e.g. capital costs. Variable costs fluctuate with the amount used, e.g. salaries, fees etc.

Remember, at the center of any academic work, lies clarity and evidence. Should you need further assistance, do look up to our Accounting and Finance Assignment Help

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start