- Subject Code : HI6026

- University : Holmes Institute My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Audit, Assurance and Compliance

Audit Assurance of Komsu Air Limited(KAL)

Table of Contents

Question 1

Question 2

Question 3

Question 4

Question 5

References

Question 1

Question 2

a) Auditor’s Expectation

-

Installation of new system software; namely, Data Base Management System

-

Modification in business programs and events, which can only be authorized with specific consent. It can be password protected

-

Entire modifications in specific programs must be considered with a higher supervision

Therefore, the auditor is not dependable on the earlier software because of the alteration in it. The adaption of new or innovative software on the ongoing basis of the previous system has made it more unreliable for the auditor. The system has been altered largely in the past as well as the present (Adler et al., 2018).

b) For a better performance to take place in the company or for a better future, an auditor should conduct the auditing process more often at least once after every month. However, in the given case, there is an update of the software in the month of April. As the auditor was not sure about the past system, it is recommended that after the installation of the new system, an auditing process should be taken place, as it will be more feasible and trustworthy for the auditor.

c) Inventory control system records numerous transactions in a business, and the process of inventory system is executed by most of the companies to preserve sufficient stock to fulfil the demand related to future and present. However, the interim audit is highly affected by many factors such as return on sales, debtors’ increment, cash sales of inventory, and sale on credit basis. Therefore, it can be concluded that interim audit cannot end the financial image because there are many transactions, taking place throughout the year and cannot be concluded at an interim date due to certain transactions. At the end of the period date, many factors influence the operations that are recorded (Kearns et al., 2018).

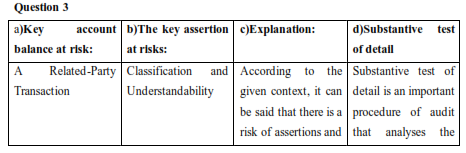

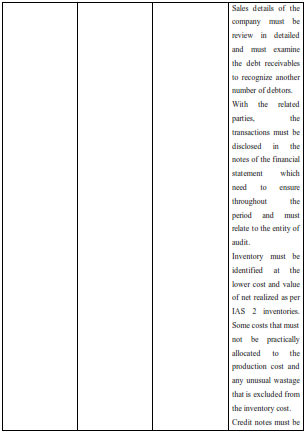

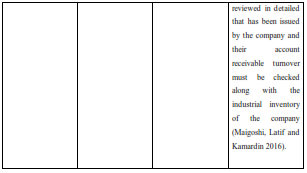

Question 3

Question 4

a) Key audit matters: In the context of key audit matters (KAM), the change in the auditor reporting standards plays a significant role. The introduction of ISA (International Standard on Auditing) 701brought change in the independent auditor's report to improve the make the key audit matters work more efficiently. Due to the application of ISA 701, two types of audits are considered- audit of listed entity’s financial statement and the time when auditor feels to involve key audit matters in the report of auditor (Klueber, Gold and Pott, 2018). KAM are considered as those matters that are significant in the case of professional judgment of the auditor and financial statement of a company's current period. In the context of KAM, the auditor mainly takes into account:

The financial statement that is related to strong management judgment and includes the estimation of accounting related to high estimation uncertainty.

The areas in which material misstatement risk is discovered or other significant risks that are included in the revised version of ISA 315. Risks that are identified and assessed after the analysis of the company and its environment.

Any problems occurred due to the audit of any transaction or event that is significant for the entity and problem regarding that occurred during the specific time.

The impact of KAM on audit report format: The key purpose of involving KAM is to enhance the auditor report’s communicative value because KAM provides more transparency regarding an audit that is performed (Ratzinger-Sakel and Theis, 2017). The addition of key audit matters in the auditor report provides additional information to assist the users to understand the matters of professional judgment.

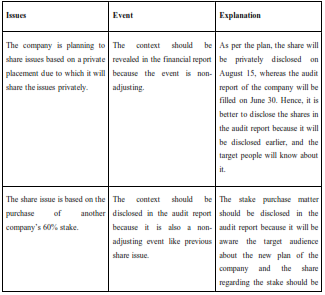

b) Analysis of the Case

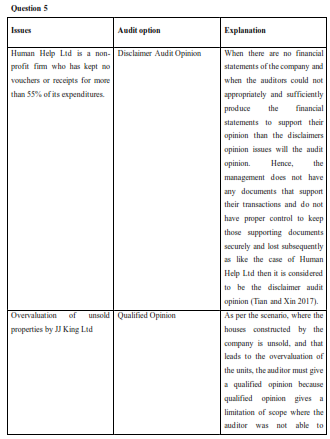

Question 5

References

Adler, P., Falk, C., Friedler, S.A., Nix, T., Rybeck, G., Scheidegger, C., Smith, B. and Venkatasubramanian, S., 2018. Auditing black-box models for indirect influence. Knowledge and Information Systems, 54(1), pp.95-122.

Bona-Sánchez, C., Fernández-Senra, C.L. and Pérez-Alemán, J., 2017. Related-party transactions, dominant owners and firm value. BRQ Business Research Quarterly, 20(1), pp.4-17.

Heliodoro, P.A., Carreira, F.A. and Lopes, M.M., 2016. The change of auditor: The Portuguese case. Revista de Contabilidad, 19(2), pp.181-186.

Karneyeva, Y. and Wüstenhagen, R., 2017. Solar feed-in tariffs in a post-grid parity world: The role of risk, investor diversity and business models. Energy Policy, 106, pp.445-456.

Kearns, M., Neel, S., Roth, A. and Wu, Z.S., 2018, July. Preventing fairness gerrymandering: Auditing and learning for subgroup fairness. In International Conference on Machine Learning (pp. 2564-2572).

Klueber, J., Gold, A. and Pott, C., 2018. Do Key Audit Matters Impact Financial Reporting Behavior?. Available at SSRN 3210475.

Maigoshi, Z.S., Latif, R.A. and Kamardin, H., 2016. Earnings management: A case of related party transactions. International Journal of Economics and Financial Issues, 6(7S).

Ratzinger-Sakel, N. and Theis, J., 2017. Does considering key audit matters affect auditor judgment performance?.

Saidin, S.F., Malek, M., Ibrahim, D.N. and Kee, P.L., 2016. Events after Reporting Period and Misstatements in Quarterly Accounts. International Journal of Economics and Financial Issues, 6(7S).

Tian, J. and Xin, M., 2017. Literature review on audit opinion. Journal of Modern Accounting and Auditing, 13(6), pp.266-271.

Yoon, J., Talluri, S., Yildiz, H. and Ho, W., 2018. Models for supplier selection and risk mitigation: a holistic approach. International Journal of Production Research, 56(10), pp.3636-3661.

Remember, at the center of any academic work, lies clarity and evidence. Should you need further assistance, do look up to our Audit Assurance Assignment Help

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start