- Subject Code : HI6028

- University : Holmes Institute My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Taxation Law

Calculation of Taxation Law

Table of Contents

Week 6

Week 7

Week 8

Week 9

Week 10

References

Week 6

The provisions of the Income Tax Assessment Act related to Fringe Benefit Tax provide that any payment made by the employer towards expenses of the employee would be regarded as a fringe benefit irrespective of whether the amount is reimbursed to the employee or paid directly to any third party (ATO, n.d. a). According to the facts provided in this question, as Mason’s employer has paid his course fees at Holmes Institute, this can be rightly regarded as an expense payment fringe benefit paid by the employer.

Further, the rules related to fringe benefits also provide that if the employee has been provided with any accommodation by the employer whether it is rent-free or rent is charged at less than market rates, then this shall be considered as a housing fringe benefit as per the FBT rules (ATO, n.d. b). In this case, as Mason's employer has provided him with an apartment in Brisbane at a weekly rent which is much lower than its market rent, so this can be rightly regarded as housing fringe benefit received by Mason from his employer. The amount of housing fringe benefit will be equal to the difference between market value rent and actual rent charged by his employer from Mason.

Mason's employer will be required to pay FBT on the taxable value of these fringe benefits, however, Mason will neither be required to include these amounts in his assessable income and nor pay any tax on same.

Week 7

a)

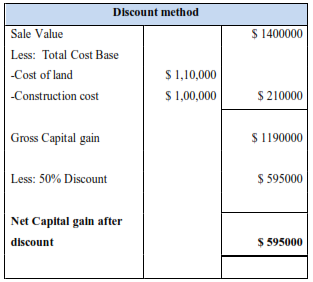

Alex's Net Capital Gain as Per the Discount Method

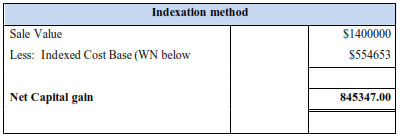

Alex's Net Capital Gain as Per the Indexation Method

Working Note:

Calculation of Indexed Cost Base

Indexed cost of land

110000*114.1/43.2 = $290532

Indexed Construction cost

100000*114.1/43.2 = $264120

Total Indexed Cost= $ 554653

b) In case this property is owned by a company and not an Individual (Alex), then the company would not be allowed choose between the two methods of calculating capital gains- Discount method and Indexation method and it would be eligible to use the indexation method of calculating capital gains only. The reason behind this is that as per the Capital gains rules of the Australian Taxation Office, the discount method of calculation of capital gains is only available to an individual, trust and complying superannuation fund and is not available for companies (ATO, n.d. c). Hence, if the owner of the property is a company, then such company will have to pay higher capital gains of $845347 only, and will not be able to choose that method which leads to lower capital gains for them.

Week 8

The Australian Taxation Office has fixed a threshold of $75000 for registration of GST which means that every business enterprise that has a turnover of $75000 or above must obtain its registration (ATO, n.d. e). Upon the registration of a business for GST, it becomes liable to charge GST on all the taxable sales made by it and also becomes automatically entitled to claim the GST input tax credit on each eligible purchase made by it from a supplier who is registered for GST. As per the facts provided in this case, Bowens Pty Ltd who is the buyer has an annual turnover of S 24 million. Moreover, Builders Choice Pty Ltd who is the supplier has an annual turnover of $ 21 million. As the GST turnover of both these companies is more than the limit of $75000 for mandatory GST registration, both these companies are required to get themselves registered for GST.

If both these companies are already registered for GST then they will be required to charge GST on all the taxable sales made by them and will be able to claim the input tax credit for all the purchases (apart from those purchases that are GST free or input taxed) made by them from GST registered suppliers. It is to be noted that if the seller has not specifically distinguished the amount of GST included in the total sales price, then it will be assumed that GST @ 10% is already included in the sale price and the sale price exclusive of GST and the amount of GST on sale will be calculated accordingly (i.e. by multiplying with 10/11 and 1/11 respectively. Thus, on the basis of above explanations, it can be concluded that the main GST consequences of these arrangements for Builders Choice Pty Ltd and Bowens Pty Ltd will be that the Builders Choice Pty Ltd will be required to charge GST on all taxable sales made by it to Bowens, and the latter will be able to claim an input tax credit of all GST paid by it on its purchases from Builders Choice. In this case, as Bowens has sold its concrete mixers @ $660 and no GST has been shown separately in invoice, then it will be assumed that GST of $60 is included in every sale of concrete mixer.

When the goods purchased in the month of October, are returned in December, then Bowens Pty Ltd will be required to show an increasing adjustment of an amount of $ 720 ( $12* 60) in its next BAS so as to reverse the GST credit that it was claimed by it on those 12 concrete mixers. Builders Choice will also have to show a decreasing adjustment in its next BAS for the same amount

Week 9

Section 47 of the ITAA 1936 tells about the tax treatment of those distributions that are made by the liquidator of a company in liquidation, to its shareholders. The section 47 says that that part of the distributions that are distributed by the liquidator of the company from the income earned by the company during the liquidation or before its liquidation will be considered as dividends paid by the company from its profits (Wolters Kluwer, n.d.). The section specifically provides that those distributions which are not made by the company from its income but are directed towards repayment of capital cannot be considered as dividends and will be assessed separately under capital gains. The capital gains rules say that a capital gain made by the shareholder upon distributions received towards repayment of capital will be subject to capital gains. However, it is to be noted that the assessee will not be allowed to claim any capital losses made on these distributions towards repayment of capital.

According to the facts of this case, Paul who is an ex-shareholder of Watson Co has received a total distribution of $ 7200 from the liquidators of the company. Out of the total distributions received by Paul, $ 3000 is unfranked dividend which is paid by the company to its shareholders according to the provisions of section 47 (1) of the Income Tax Act. Thus, it means that the amount of $ 3000 is the dividend paid by the company from income earned by it. On the basis of this explanation, $3000 will be regarded as a dividend income of Paul. Further, Paul received $4200 towards repayment of capital and the cost of shares purchased by him was $4000, leading to a gross capital gain of $200, but as Paul is an individual, he can claim the CGT discount @ 50% of capital gain; hence his net capital gain is $ 100.

Week 10

A partnership firm is not required to pay any tax on its income as all of its income is distributed among the partners in the profit-sharing ratio that has been provided in the partnership agreement. However, this does not mean that the income of a partnership firm is free of taxes. The income derived by a partnership firm is taxed in the hands of its members according to the tax rate that is applicable to their total taxable income (which includes distributions from partnerships).

It is important to consider the requirements of section 92 of ITAA for determining how much of the income of the Euca Sanitizers should be taxed in Australia. As per section 92 of the ITAA 1936, that proportion of the income of a partner from partnership firm which relates to the period during which a partner was a resident of Australia, would be regarded as regular distributions from the partnership and will be taxed in Australia (AustLII, n.d.a). This section also provides that proportion of income that is distributed to a partner who was a non-resident of Australia but the income was earned from sources in Australia, then such distribution would be regarded as regular distributions from the partnership and will be taxed in Australia only.

As per the facts of this case, the total income of Euca Sanitizers is $300000 out of which 60% is from sales in Australia while 40% is from sales in New Zealand, but as the sale in New Zealand is through business set up in Australia, the total income will be equally distributed among the partners and will be taxed in Australia.

References

ATO. (n.d. a). Housing fringe benefits. Retrieved from https://www.ato.gov.au/general/fringe-benefits-tax-(fbt)/types-of-fringe-benefits/housing-fringe-benefits/

ATO. (n.d. b). Expense payment fringe benefits. Retrieved from https://www.ato.gov.au/general/fringe-benefits-tax-(fbt)/types-of-fringe-benefits/expense-payment-fringe-benefits/

ATO. (n.d. c). The discount method of calculating your capital gain.

ATO.(n.d. d). Registering for GST. Retrieved from https://www.ato.gov.au/Business/GST/Registering-for-GST/

AustLII .(n.d. a). Income Tax Assessment Act 1997-Sect 115.25. Retrieved from http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.25.html#:~:text=(1)%20To%20be%20a%20*,months%20before%20the%20CGT%20event.

Wolters Kluwer. (n.d.). Income Tax Assessment Act 1936. Retrieved from https://iknow.cch.com.au/360document/atagUio700196sl24430314/income-tax-assessment-act-1936-section-47-distributions-by-liquidator/overview

Remember, at the center of any academic work, lies clarity and evidence. Should you need further assistance, do look up to our Taxation Law Assignment Help

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start