- Subject Code : MGT510

- University : Laureate International Universities My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Managerial Accounting

Module Assignment: Managerial Accounting Report

Contents

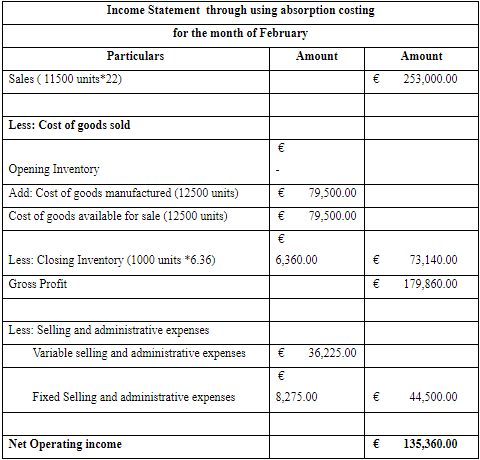

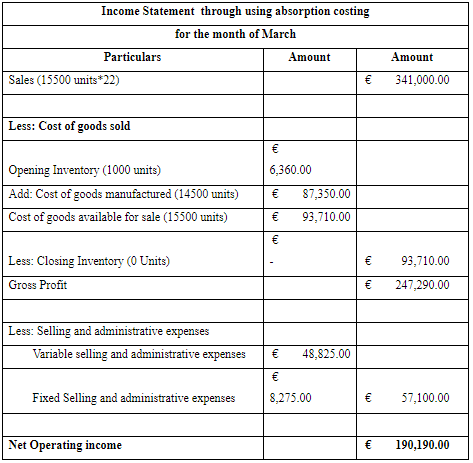

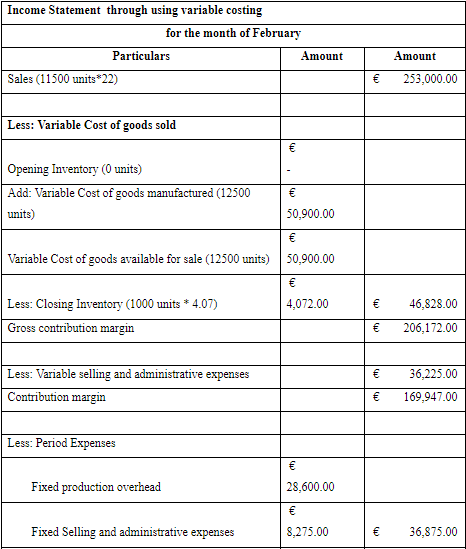

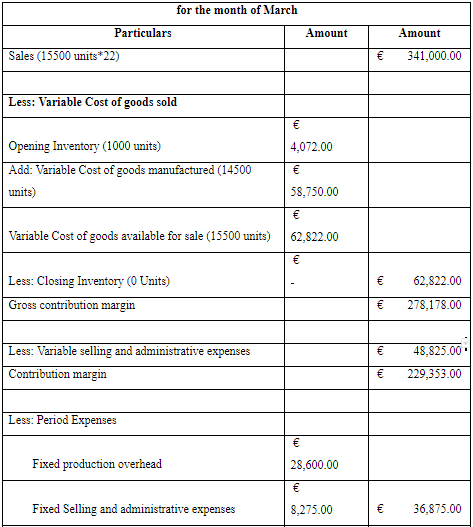

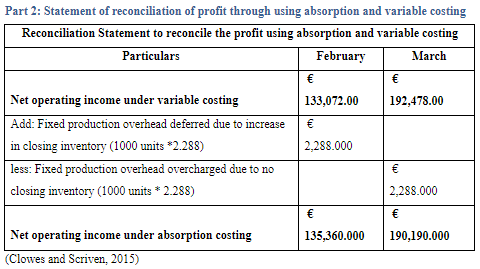

Part 2: Statement of reconciliation of profit through using absorption and variable costing

Part 4: Three ways through which Swipe 50 Ltd can improve its accounting system

Implementation of activity based costing system

Preparation of budgets and evaluating the actual results with budgeted results

Use of management accounting techniques to improve accounting system

Part 5: Role of management accounting jobs in manufacturing companies

Introduction

There is large importance of managerial accounting processes for a company as it helps in collecting, recording, analyzing and interpreting the internal accounting information that assists the business managers to take important decisions regarding its future growth and development. In this context, the present report is being undertaken for the purpose of providing an adequate understanding of the managerial accounting processes for evaluation of a company internal business processes and developing future strategic action plan. The use of different accounting methods adopted by a company for preparation of internal accounting information is explained adequately within the report.

This has been carried out in the context of a given case scenario of a company known as Swipes 50 Limited involved in manufacturing of screen protect for laptop computers, The company is emphasizing on refining its production process and the directors are placing focus on reviewing the product costing process and analyze the effects of both absorption and variable costing on the profits of a company. In this context, the report undertakes the preparation of profit statement for the company with the use of both the method by in context of the financial data given and reconciles the profit calculated with the use of both costing approaches. Also, it explains the difference between two methods and also provides suggestions to the company for improving its accounting systems. Lastly, it discusses about the importance of managing accounting jobs for a manufacturing company.

Part 3: Explanation of Difference between Absorption and Variable Costing Method and their Relative Importance

The method of absorption costing involves only allocating the fixed costs across all the units produced over an accounting period. This type of costing is also known as full costing and its involves treating the costs of all manufacturing components such as direct material , direct labor, variable overhead and fixed overhead in the product costs as per the generally accepted accounting principles (GAAP). This method of costing allocates the fixed overhead costs across all the units manufactured and thus helps in determining of per-unit cost. It generally results in identifying the two categories of fixed overhead costs, that includes cost of goods sold and inventory costs. The major importance of using absorption costing method is that it enables the companies to develop a suitable pricing policy that includes fixed and variable manufacturing costs. It ensures that prices are determines on the basis of all the cost incurred in the production process. It avoids the separation of costs into fixed and variable that cannot be done in an easy and accurate manner. In addition to this, the method of accounting also helps in determining accurate profitability as all the sales and marketing expenses are recorded under the same period. However, the major drawback associated with this method is that some of the period costs does not have any future relevance and thus should not be included within the cost of product and inventory (Lalli, 2011).

On the other hand, variable costing involves including only the variable costs that is incurred in the production process. This type of costing method involves emphasizing only variable production costs for costing of products and valuation of inventory. This type pf costing unlike absorption costing integrates all fixed overhead costs into a single expense and reports them into a single line item on the balance sheet. The major benefit of using variable costing as compared to the absorption costing is that it enables only in identifying the significant costs that were actually incurred in developing a product or service. Also, this type of costing helps in developing income statement by the use of contribution margin that leads in attaining better information in context of cost volume profit analysis (CVP) analysis. The absorption costing does not help in undertaking a CVP analysis. However, the major drawbacks associated with the use of this method is that it does not help in determination of actual process of products for companies as it does not involve allocation of fixed costs to the production. Also, the use of this costing method leads in attaining lower net income for a company because all fixed costs are reported in the same period in which they are incurred (Maingi, 2013).

It can be stated on the basis of analysis of difference between the above two methods of cost accounting that variable costs accounting seems to be more adequate for decision-making purposes of the business managers. This is because it helps in providing an adequate analysis of cost and volume as it adequately helps in determining the variation in costs that can occur at different levels of production. Thus largely assist the business mangers to analyze the operational efficiency and develop future strategies to improve the operational effectiveness. Also, the method of costing can be regarded as more suitable for the companies that are involved in manufacturing of different line of product (Maingi, 2013). This is because it is largely easy to identify the differences in profits involved in producing one items to that of another by only analyzing the differences in the variable costs of production. It is also associated with less chances of causing manipulation in the financial reporting for the general users as it does not result in inflating a higher net income that generally results in using the method of absorption costing. On the other hand, some of the accountant argues that absorption costing takes into account all the cost of production that includes fixed and variable and therefore helps in providing a better picture of production cost that can better help the company management in valuating profitability and determining process. Also, the method of costing is in compliance with IFRS and GAAP and therefore regarded to be more suitable to be used in financial reporting as compared with that of variable costing (McWatters and Zimmerman, 2015).

However the business managers still largely adopts the use of variable costing for conducting break-even analysis, determining the contribution margin and enhancing the decision-making in context of improving the operational efficiency. It can be stated on the basis of analyzing the important characteristics of both the costing method that variable costing should largely be applied by the business companies that are involved in manufacturing of diversified product lines. This is because it largely assists in determining the profits attained from each of the product line in an accurate manner. On the other hand, the firms that are involved in developing a single product line can adopt the use of absorption costing as the method help in determining accurate price level on per unit basis of products manufactured. This is because all costs are absorbed by the products that are manufactured in the method of absorption costing. However, as per the accountings standards firms are allowed only for adopting the sue of absorption costing as variable costing seems to contradict the matching principle which states that all related revenue and expenses should be recognized within the same accounting period. However, in the method of variable costing does not involve allocation of fixed manufacturing overhead and thus is not allowed for external reporting purpose. As such, it is largely used by the business managers for decision-making purposes related to improving the operational effectiveness (Moles and Kidwekk, 2011).

Part 4: Three ways through which Swipe 50 Ltd can improve its accounting system

Management accounting system is an important category of complete accounting system and improving the process of management accounting system will directly improve the accounting performance of an entity. The main purpose of management accounting system is to provide sufficient quantitative and qualitative information on company’s operational as well as financial performance. Management accounting provides information to the managers or owners of the company and helps them to make the economic decisions through use of budgeting technique and apply controls on the variances noticed from actual result and budgeted results. So, company can use management accounting as a resource planning tool as it focuses on future and it can also be used as instrument for controlling resources due to its ability to focus on present. So, it can be said that way to success and to increase profitability performance of any entity it is important to build rigorous management accounting system that ensure all the cost elements are in place and are properly controlled (Rasmussen, 2013).

In the given case it was clear that Swipes 50 Limited has already implemented the management accounting system that provide required information to managers for making important economic decisions. Although not much detail have been provided by the company about its management accounting system but it is assumed that company uses simpler form of management accounting system which is not providing detailed information to improve the profitability performance. Three important ways through which Swipes 50 Limited can improve its management accounting system is given below:

Implementation of activity based costing system

As it is clearly reflected from given information that company manufactures only one product and all the overhead cost have to be directly applied to that one product but there might be chance that some of overhead costs are not linked with product and take place with no reason. So, after implementation of activity based costing system, cost from each department will be separated and only those overhead costs are being added to the product that has any relation with product. It will help to separate value added costs and non value added costs from the total overhead costs. Through the application various costing techniques non value added activities can be reduced and it will help to improve the overall profitability of the company. In addition to this activity based costing will provide information that can used to calculate the exact profitability of each of product manufactured by an organization. So, in case if Swipes 50 Ltd adds one more line of product it will be easy for the company to distribute the overhead costs on the basis of usage by each one of product (Scheller-Kreinsen and Geissler, 2009).

Activity based costing is much more reliable and accurate cost allocation method as compared to absorption costing. Absorption costing takes the full amount of manufacturing overhead and spread evenly to the production quantities of all products taken together. So, there may be case that certain products have utilized only some of overhead costs as compared to other. This issue can be easily resolved through use of activity based costing system. Activity based costing help to calculate the accurate product cost as it makes focus on the cause and effect relationship of cost incurred. It takes into accounts the activities that are taken place within the organization and calculate per unit cost of overhead through use of suitable cost driver. Cost driver is selected on the ground that it can be quantified and relate to respective overhead cost. ABC costing makes use of cost driver to allocate the overhead costs to each product on the basis of number of driver units absorbed by respective product. Overall it can be said that ABC costing is superior as compared to absorption costing method as it make use of relevant cost drivers for allocating overhead costs. On the other hand, absorption costing makes use of only single cost driver to allocate the overall manufacturing overheads (Shim, Siegel and Shim, 2011).

Preparation of budgets and evaluating the actual results with budgeted results

Management accounting system is not a one day process and no company can succeed without proper budgets and future plan. Budgeting is an important part in the process of planning and control of management accounting system. Management accounting system requires a base to evaluate the actual results in order to evaluate the performance of each department and take actions to eliminate the variance. In other words it can be said that budget provide a regulatory framework that can be used to develop the plan of action, to minimize the future uncertainties, to calculate the future costs and revenue and to think to future events. Budget is an integral part of management accounting system and it is essential to achieve the goals and objectives of an organization (Tănase, 2013).

Budgeting can be used to achieve the target profit at desired level of volume through controlling the non value added costs incurred during the budgeted year and focusing on total quality management. Budget ensures that costs are allocated to only those activities that help to achieve the strategic objectives of organization. Budgets can be used to evaluate the target performance of manager and held liable those with charge in case the desired level of profit is not achieved. The process of drafting the budget gives opportunity to each department to provide their recommendations and contribute towards the organization vision. A well drafted budget help manager of each department to allocate the duties and responsibilities properly to each team member.

Budgeting will improve accounting system as it is the most important part of internal control system and can be used to compare the actual results with budgeted results to calculate the variance. It will help managers to take further steps to eliminate the unfavorable variances and try to achieve the favorable variances to improve the profitability performance (Vanderbeck, 2012).

Use of management accounting techniques to improve accounting system

There are many management accounting techniques that can be implemented to integrate the management performance with the financial performance of the company. Management accounting techniques such as variance costing, cost volume profit, standard costing, and marginal costing and cash flow management will help Swipes 50 Limited to evaluate different aspects of costing information and integrate resultant data with the financial performance of company. For example, cost volume profit analysis with provide information on breakeven units and also provide numbers of units required to be sold to achieve the target profit.

Part 5: Role of management accounting jobs in manufacturing companies

The role of management accountant is take part in managerial planning and decision making process through evaluating the financial information and through undertaking related accounts administration. Following are the different roles and responsibilities of management accountant in any manufacturing firms:

-

To prepare the reports, budgets and financial statements

-

To undertake the managerial administration and internal audits

-

Communicating the essential details to the staff members to ensure management effectiveness

-

To forecast and control the income and expenditures

-

To participate in formulation of business strategies to deliver business objectives of wealth maximization

-

To deal with inventory management and ensure proper supply chain management

-

To perform various costing functions to ensure breakeven and target profit is achievable (Arnold, 2013)

Management accountant performs following important managerial functions in manufacturing company:

-

Make or buy decisions: The decision to make or buy helps to determine which products to be manufactured in-house and products that should be brought from the suppliers. It is not easy for normal accountant or manager to determine the cost structure when products are manufactured in-house and similar product purchased from outside. Here, role of management accountant arises as he can understood cost structure in much better way as compared to any other accountant (Zimmerman and Yahya-Zadeh, 2011).

-

Relevant costing: In manufacturing companies there is need to make decisions on selection of projects to achieve the maximum profits. In the decision making process there is need to focus on relevant cost and ignore the irrelevant cost. Only the management accountant has the ability to understand which costs can be regarded as relevant and costs that can be regarded as irrelevant.

-

Variance Costing: GAAP requires all the cost of production must be assigned to products manufactured by the company. In case when the number of products manufactured differs from the products sold, there arises a case of distortion in reported accounting profit and actual profit earned by the company. So there is need to adjust the overapplied or underapplied costs in order to determine the actual profit and variance between them (Schlichting, 2013).

Conclusion

Management accounting is most important part of accounting system as it helps to formulate the budgets, calculate variance and determine products cost. Management accounting comprises of various costing techniques such as make or buy decisions, target costing, cost volume profit analysis, activity based costing, inventory management and many other that helps to improve the accounting system.

References

Adler, R. (2013). Management Accounting. UK: Routledge.

Arnold, G., (2013). Corporate financial management. USA: Pearson Higher Ed.

Berman, K. (2015). Financial Planning, Budgeting, and Forecasting: Financial Intelligence Collection. UK: Harvard Business Review Press.

Clowes, R. & Scriven, V. (2015). Budgeting: A Practical Approach. Pearson Higher Education AU.

Lalli, W. (2011). Handbook of Budgeting. US: John Wiley & Sons.

Maingi, J. (2013). Advantages & Disadvantages of activity based costing with reference to economic value addition. Germany: GRIN Verlag.

McWatters, C., & Zimmerman, J. (2015). Management Accounting in a Dynamic Environment. UK: Routledge.

Moles, P. & Kidwekk, D. (2011). Corporate finance. US: John Wiley &sons.

Rasmussen, N. et al. (2013). Process Improvement for Effective Budgeting and Financial Reporting. US: John Wiley & Sons.

Scheller-Kreinsen, D. & Geissler, A. (2009). The ABC of DRGs. Euro Observer 11(4), pp. 1-5.

Schlichting, T. (2013). Fundamental Analysis, Behavioral Finance and Technical Analysis on the Manufacturing companies. Australia: GRIN Verlag.

Shim, J.K., Siegel, J.G. & Shim, A.L. (2011). Budgeting Basics and Beyond. US: John Wiley & Sons.

Tănase, G.L. (2013). An Overall Analysis of Participatory Budgeting: Advantages and Essential Factors for an Effective Implementation in Economic Entities. Journal of Eastern Europe Research in Business and Economics.

Vanderbeck, E. (2012). Principles of Cost Accounting. Cengage Learning.

Zimmerman, J.L. & Yahya-Zadeh, M., (2011). Accounting for decision making and control. Issues in Accounting Education, 26(1), pp.258-259.

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start