- Subject Name : Taxation Law and Compliance

Assignment: Capital Gain Tax (CGT)

Contents

Part 1) Explaining the timing of the CGT events in both the two cases

Part 2) Net capital gains (losses) to be included in Harrison Carter’s tax return

Transactions

The following transactions have been taken place that results in capital gain events

-

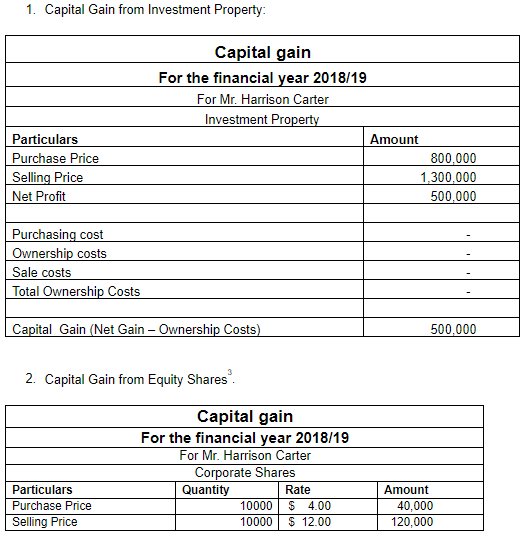

First transaction: Investment Property

-

Harrison Carter who is an Australian resident has acquired or purchased an investment property, at market value, on 24 January 1999.

-

He paid a 10% deposit of $80,000 that means the acquired rate is $ 800,000

-

The balance amount of $720,000 was paid on 5 December 2001 and the title transferred in his name. Harrison Carter was recorded as the registered proprietor.

-

During December 2001, the market value of the property was $1m.

-

Harrison Carter sold the property on 14 June 2018 for $1.3m

-

Second transaction: Investment in Equity Shares

-

Harrison Carter acquired 10,000 shares in Star Entertainment Ltd in October 1985

-

The purchase was made at a rate of $ 4 per share

-

Decided to sell the shareholding and signed a share transfer document and handed the transfer and share script to the Stock Exchange on 20 June 2018

-

The Sales was made at a rate of $ 12 per share

-

The transfer was not registered with Star Entertainment Ltd until 10 July 2018.

-

Harrison Carter incurred a capital loss in 2018/19 amounting to $65,000.

Part 1) Explaining the timing of the CGT events in both the two cases

Transaction 1: Generally, the time you acquire a CGT asset (your acquisition date) is when you become its owner, most commonly because you've bought it or received it as a gift.

However, there are two common situations where your acquisition date is likely to be different from the date you become the owner:

-

When you buy an asset under contract and don’t take immediate possession, such as with real estate – in this case your acquisition date is the time you enter into the contract (normally the date on the contract) and not the date of settlement (except for certain transfers to trusts)

-

When you inherit a CGT asset – in this case the acquisition date is the date of death of the person who bequeathed it to you.

Ans.: Hence the timing of a CGT event will be the date of 14 June 2018 when he sold the property and the date of acquire is when Harrison Carter enter into a contract to purchase the property which is 24 January 1999 and not the date of settlement which is 5 December 2001

Transaction 2: The CGT event took place on the date of 10 July 2018.

CGT was introduced on 20 September 1985 and Harrison purchased the shares in October 1985, hence it will be the date of acquiring the securities.

Part 2) Net capital gains (losses) to be included in Harrison Carter’s tax return

Net Capital Gain or Loss

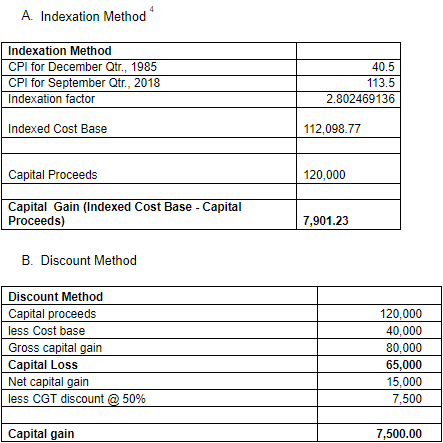

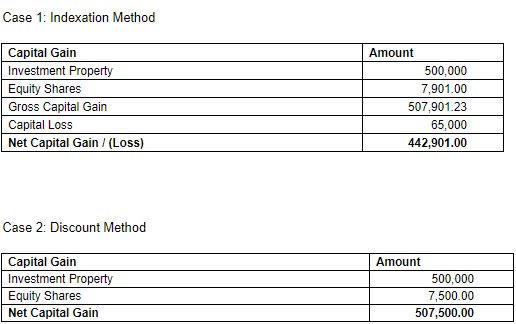

Advice: It is clearly evident from the above tables that indexation method is more beneficial to Harrison for calculating the capital gains as with indexation method the net capital gains coming after adjusting for the previous year’s capital losses is comparatively lesser. With the indexation method, Harrison has made capital gain in the following two securities:Case 2: Discount Method

-

Capital gain tax from investments is $ 500000

-

Capital gain tax from shares is $ 7901

Hence net capital gain after making adjustments to previous year’s capital loss of $ 65000 is $ 442,901.00. While the capital gain calculated using the discounted method is much higher amounted to $ 507500.

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start